|

Edition 06 |

The Bitcoin newsletter for Kiwi stackers

|

The Mullet Data Centre

|

|

Business in the back, AI up front. How public Bitcoin miners stopped mining Bitcoin - and what's quietly happening to the network as a result.

|

|

In early February, the CEO of Bitfarms - a top-ten public Bitcoin miner with operations across North America - said the quiet part out loud. "We are no longer a Bitcoin company." The same statement announced that Bitfarms was redomiciling from Canada to the United States and rebranding entirely. The new name? Keel Infrastructure.

That should have been a bigger story than it was. Because Bitfarms isn't an outlier. It's the leading edge of a structural shift that has, in the space of about nine months, transformed what publicly listed Bitcoin miners actually do for a living.

The headline figure from CoinShares' Q1 2026 report: by December this year, up to 70% of public miner revenues are projected to come from AI and high-performance computing - up from roughly 30% just two quarters ago. The pivot is being funded by an extraordinary liquidation. Public miners sold more than 32,000 BTC in Q1 2026 alone, more than they sold across all four quarters of 2025 combined. Marathon offloaded 15,133 BTC in March on its own. The cash isn't going into more ASIC rigs. It's going into GPU racks, retrofitted cooling, and contracts with hyperscalers.

So what happened, and what does it mean for the network you store your savings on?

|

|

$70B+

AI/HPC contracts

announced

|

|

|

32,000

BTC sold by public

miners in Q1 2026

|

|

|

70%

Projected AI share of

miner revenue by EOY

|

|

|

Why the math broke

Three things happened at once. The April 2024 halving cut block rewards in half - a planned event, but a real one. Bitcoin's price then fell from $126,000 in October 2025 to around $60,000 in February 2026, cutting miner revenue per joule again. Energy costs didn't move. Hardware financing didn't get cheaper. The result was a margin squeeze that turned a chunk of the public sector into structurally loss-making operations.

Meanwhile, the AI compute market exploded. Hyperscalers and AI-native operators - Microsoft, Oracle, CoreWeave - were paying for GPU capacity on multi-year contracts at margins Bitcoin miners hadn't seen since 2021. Profit per megawatt for GPU hosting overtook profit per megawatt for SHA-256 hashing. And it turned out that public miners had three things hyperscalers urgently wanted: land, power contracts, and substations.

They didn't pivot because they wanted to. They pivoted because the spreadsheet told them to.

|

|

Chart 1

Public miner revenue mix: the great flip

|

Q4 2025

Today

|

|

Bitcoin mining 70%

|

AI 30%

|

|

|

PROJECTED FLIP ↓

|

|

End 2026

Forecast

|

|

| |

Dominant revenue line

|

|

Secondary revenue line

|

|

Source: CoinShares Q1 2026 Mining Report.

|

|

The Mullet Strategy

The metaphor that's gone viral in mining circles is the "Mullet Data Centre." Business in the back, party in the front - except inverted. AI lives at the front of the building under multi-year contracts at stable dollar margins. Bitcoin mining lives at the back, soaking up whatever capacity isn't on a GPU lease.

The appeal is obvious. AI clients sign 5, 10, 12, 15-year contracts at 85% EBITDA margins. IREN's deal with NVIDIA alone is worth $3.4 billion over five years. Bitcoin hashing, by contrast, is a one-day contract with the network that you re-sign every block. From a capital allocator's perspective, the AI revenue line stabilises the business and gets the multiple re-rated.

The market has noticed. Miners with secured HPC contracts now trade at 12.3 times next-twelve-month sales. Pure-play miners trade at 5.9x. The market is paying more than double for AI exposure, which is the strongest possible incentive to pivot further.

|

|

Chart 2

The public miners pivoting to AI

|

TeraWulf (WULF)

$12.8B contracted HPC revenue

|

|

|

Core Scientific (CORZ) + CoreWeave

$10.2B over 12 years. Already 39% of revenue from AI colocation in early 2026.

|

|

|

Hut 8 (HUT)

$7B, 15-year AI infrastructure lease (River Bend campus)

|

|

|

IREN (Iris Energy) + NVIDIA

$3.4B, five-year deal. Aggressive site-by-site retrofitting underway.

|

|

|

Bitfarms (BITF) → Keel Infrastructure

Exploring 341 MW of capacity to pivot away from crypto mining

|

|

|

Cipher Mining (CIFR)

AI infrastructure agreements signed, including with Fluidstack

|

|

|

Cango Inc. (CANG) → EcoHash

Rebranding entirely as an AI infrastructure provider

|

|

Not exhaustive. Total announced AI/HPC contracts across the public miner cohort now exceed $70B.

|

|

|

"We are no longer a Bitcoin company. We are an infrastructure-first owner and developer for HPC/AI data centres."

Ben Gagnon, CEO — Bitfarms (now Keel Infrastructure)

|

|

What's actually leaving the network

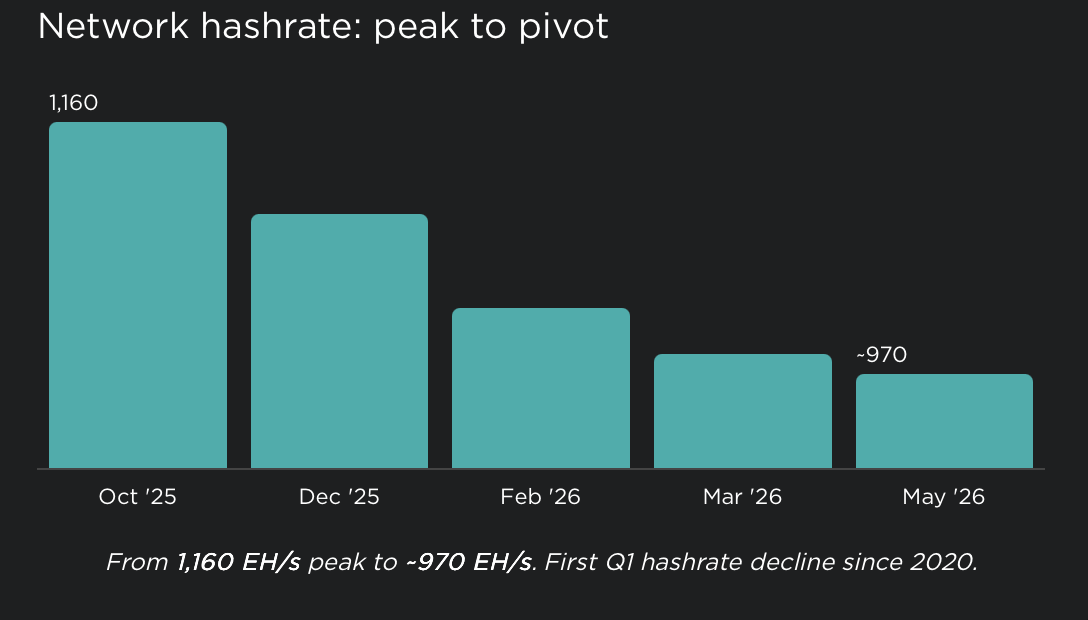

Total network hashrate has fallen from its peak of 1,160 EH/s in October 2025 to roughly 970 EH/s as of mid-May 2026. That's the first Q1 hashrate decline since 2020 and the longest sustained period of net decline since the China mining ban in 2021. Bitcoin's difficulty has adjusted downward to compensate, which is exactly what it's designed to do. The network is fine.

But the composition of who runs the network is changing fast.

|

|

Chart 3

Network hashrate: peak to pivot

|

|

| |

|

Oct '25

|

Dec '25

|

Feb '26

|

Mar '26

|

May '26

|

|

|

From 1,160 EH/s peak to ~970 EH/s. First Q1 hashrate decline since 2020.

|

|

|

|

What's leaving is publicly listed, US-based, industrial-scale mining. What's not leaving: sovereign-backed miners (Bhutan, El Salvador, UAE, parts of LATAM and Africa), private operators, mid-scale efficient miners on sub-15 J/TH gear, off-grid stranded-energy operations, and home and retail miners.

And here's the bit that hasn't been priced into the discussion yet: for the operators who stay, hashprice goes up. Less competition for the same coinbase reward means a higher slice of the pie for everyone still at the table. Bitmain's S23 series and Bitdeer's SEALMINER A3, both operating below 10 joules per terahash, are reaching scale through the first half of 2026 - which keeps the economics workable even at current prices.

|

|

The decentralisation paradox

For most of the last cycle, the running concern about Bitcoin mining was concentration - too much hashrate in the hands of US public miners, too much risk of regulatory capture. The AI pivot is, somewhat accidentally, a decentralisation event. As US publics exit pure-play hashing, sovereign miners, private operators, and mid-scale efficient miners pick up the slack. Geographic and political distribution of hashrate is increasing, not decreasing. That's good news for the network, even if the headline hashrate number stays soft for a while.

|

|

The energy market wrinkle

There's one more thread worth pulling, and it's the thing we'll dig into properly next edition.

Bitcoin mining is a uniquely flexible electrical load. You can switch it off in seconds, and the network just adjusts difficulty downward to compensate. That property is hugely valuable to grid operators trying to balance variable renewable generation - wind and solar that arrive whether the grid wants them or not.

AI data centres are the opposite. They demand 99.99% uptime under contractual obligation. Microsoft isn't going to let CoreWeave switch off a training run because the wind dropped. Which means the megawatts now being pulled into AI buildings are, in effect, becoming inflexible load.

The implication is interesting. The more megawatts that flip from mining to AI, the harder it gets for grid operators to balance renewables - and the more curtailed (wasted) energy there is sitting on the table for whoever is willing to be the buyer of last resort. That buyer, structurally, is still Bitcoin. We'll come back to this.

|

| |

|

The NZ angle

What this means for Kiwi stackers

Aotearoa isn't a hyperscaler market. We don't have the data centre gravity of Northern Virginia or West Texas, and our grid isn't competing with Microsoft for megawatts. What we do have is an 80%+ renewable mix with real variability - hydro storage, growing wind, increasing solar - and a Bitcoin price that, for Kiwi stackers, is the same global asset whether it's secured by a Texan public miner or a Bhutanese sovereign one.

The takeaway for the Stacked community is straightforward. The network you're storing your savings on is becoming more geographically distributed, not less. The companies that have been loudest in the mining narrative are the ones leaving. The ones picking up the slack are smaller, more private, more distributed, and considerably harder to lean on politically. That is healthier.

And if you ever wondered whether Bitcoin mining was just a stepping stone to AI infrastructure - that's now provably backwards. AI infrastructure is what mining facilities became when no one was looking. The fact that you can still do the original thing on the same boxes is the feature, not the bug.

|

|

|

Stack accordingly,

Simon

Co-founder & CRO, Stacked

|

|

stackedbitcoin.com · FSP1005773 · Aotearoa New Zealand

You're receiving this because you signed up at stackedbitcoin.com.

Unsubscribe · Update preferences

|

|